An updated version of the draft ESRS (European Sustainable Reporting Standard) was published in June. This had been accompanied by a public consultation which was accepting feedback until 7 July, with final delegated act to be published within this month.

This article outlines the content of the updated version.

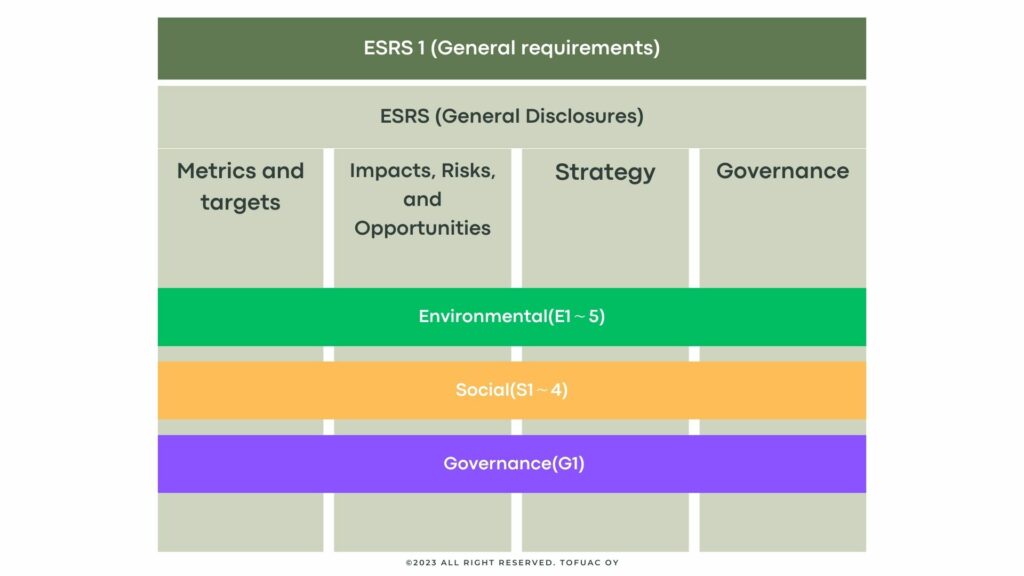

The structure of ESRS

Before we guide you about the content of the updated version, we would like to reiterate the structure of the ESRS standards.

ESRS 1 and 2 are mandatory reporting requirements for all companies as a general principle.

ESRS 2 consists of four disclosure requirements: ‘Governance’, ‘Strategy’, ‘Impacts, risks and opportunities’ and ‘Metrics and Targets’.

For these four requirements, there are three topic-specific disclosure requirements for ‘environment’, ‘society’ and ‘governance’ (cross-cutting standards).

The key changes to the ESRS standards

Broadly speaking, the following five contents have been updated.

1, Materiality

All disclosure requirements are subject to the materiality assessment is mandatory.

However, if climate change is deemed not a material topic, a detailed explanation of the conclusions of the materiality assessment is required. They are also required to disclose a table of all datapoints derived from EU legislation, evidencing where they are located and, if not, indicating that they are ‘not material.

2, Additional phasing-in

2-1 All undertakings

In the first year, the following information may be omitted

- Anticipated financial impacts related to environmental issues other than climate change (ESRS E2/E3/E4/E5).

- Specific data points related to ESRS S1 ‘Own employees’ (social protection,persons with disabilities, work-related ill health, and work-life balance).

2-2 Undertakings with less than 750 employees

The following items may be phased in

Exemptions in the first year of application of the standard

- Scope 3 GHG emissions data

- Disclosure requirements for ESRS S1 ‘Own employees’

Exemptions for in the first two years of application of the standard

- Disclosure requirements for ESRS E4 ‘Biodiversity and Ecosystems’

- All non-own workforce standards (ESRS S2/S3/S4)

- Disclosure requirements specified in the standards on biodiversity and on value-chain workers

- Affected local communities

- Disclosure requirements specified in the standard on consumers/end-users

To allow time for adaptation to the disclosure requirements, particularly complex disclosures (e.g. collection of indirect information on supply chains, financial impacts, etc.) will be phased in as described above.

3, “Mandatory” to “Voluntary” disclosures

- Biodiversity Transition Plan and specific indicators on ‘non-employees’ in the undertaking’s own workforce

- An explanation of why the undertaking may consider certain sustainability topics not to be material.

4, Additional flexibility in certain disclosures

- Requirements on financial effects arising from sustainability risks and on engagement with stakeholders

- Disclosure requirements on stakeholder engagement in the methodology used for the materiality process

- In ESRS G1 ‘Business Conduct’, revised data points on corruption and bribery and protection of whistleblowers who may be deemed to have violated their right not to commit self-crime

5, Other

- Coherence with EU regulatory framework

- Improved interoperability with global standard-setting initiatives, including GRI and ISSB

- Other editorial changes

The biggest change in this updated version is the additional phase-in. The change from the European Commission’s idealistic standards to realistic standards will be a great relief for reporting companies, including those in Europe.

As mentioned at the beginning of this article, final delegated act to be published as early as during July. We will keep to further developments in the ESRS. Stay tuned!

Photo by Markus Winkler on Unsplash